Homeowners Insurance Pennsylvania: 10 Things Every PA Resident Should Know Before Buying

- Jeff Owens

- Feb 13

- 6 min read

Buying a home in Pennsylvania is exciting, and let's be honest, a little overwhelming. Between mortgage paperwork, inspections, and settlement dates, homeowners insurance can feel like just another checkbox. But here's the thing: it's one of the most important decisions you'll make as a homeowner.

I've spent years helping Pennsylvania residents navigate homeowners insurance, and I want to share what I've learned. Whether you're buying your first home in Pittsburgh or refinancing in the Poconos, these 10 insights will help you make confident, informed decisions about protecting your biggest investment.

1. Pennsylvania Doesn't Require It (But Your Lender Does)

Here's something that surprises people: Pennsylvania has no state law requiring homeowners insurance.

But don't celebrate just yet. If you have a mortgage, which most of us do, your lender will absolutely require it. They're protecting their investment, and honestly, you should want to protect yours too. If you own your home outright, insurance is technically optional, but I can't imagine recommending going without it. One kitchen fire or burst pipe, and you're facing tens of thousands in out-of-pocket costs.

The bottom line? Think of homeowners insurance as non-negotiable, regardless of what Pennsylvania law says.

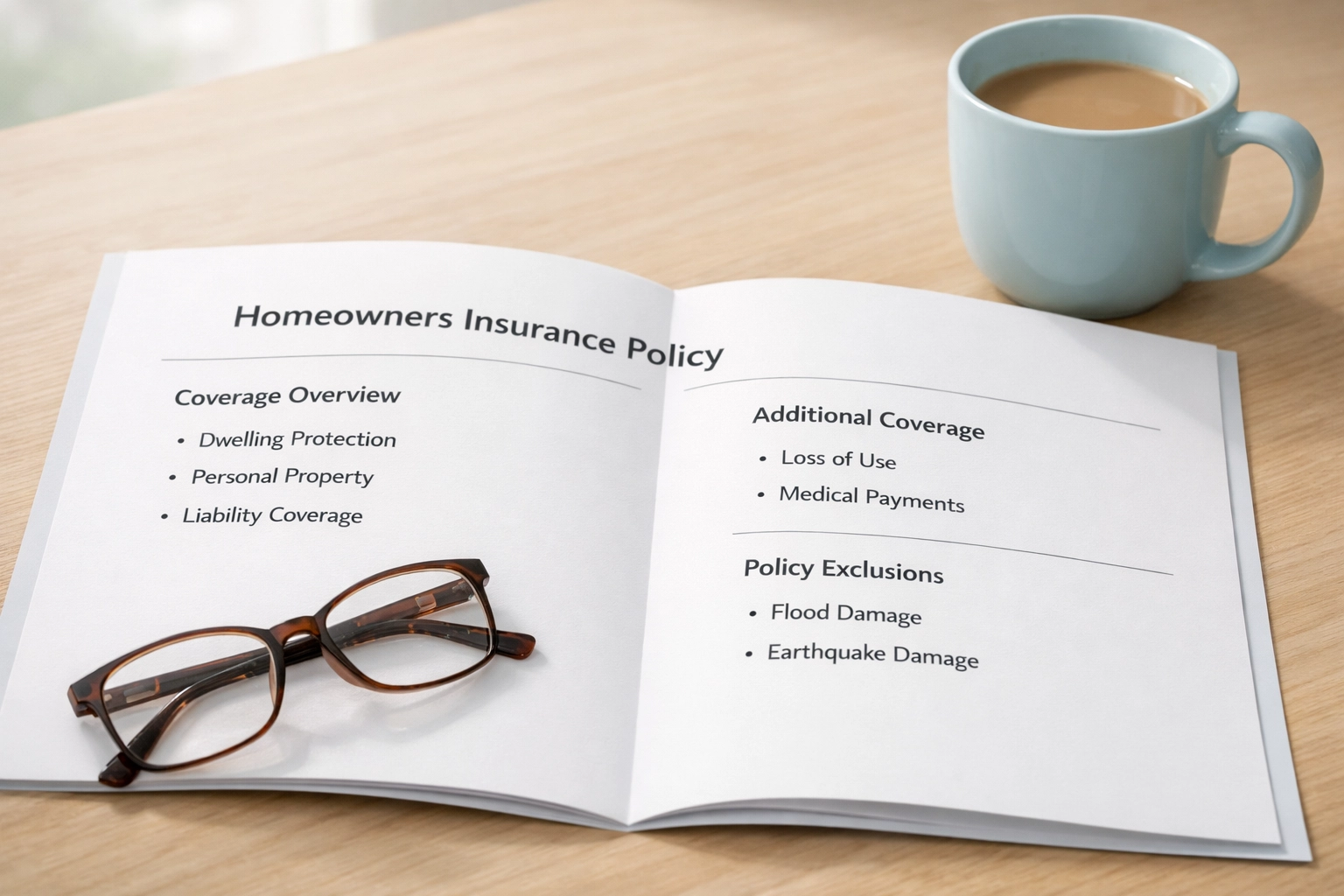

2. Know What's Actually Covered in Your Policy

Not all homeowners policies are created equal, and I've seen too many people discover gaps in coverage after it's too late.

A standard Pennsylvania homeowners policy typically includes:

Dwelling coverage: Your home's structure, walls, roof, foundation

Personal property coverage: Your furniture, electronics, clothing, and belongings

Liability protection: If someone gets injured on your property

Medical payments: Guest injuries, regardless of fault

Loss of use: Temporary housing if your home becomes unlivable

Other structures: Detached garages, sheds, fences

Understanding these components helps you evaluate whether you're adequately covered. I always encourage clients to review each section carefully and ask questions. Your policy should make sense to you, not just your insurance agent.

3. Replacement Cost vs. Actual Cash Value, Know the Difference

This one's huge, and it can save you thousands when filing a claim.

Pennsylvania insurers must offer replacement cost coverage, which reimburses you for the full cost to replace damaged items at today's prices. The alternative? Actual cash value coverage, which factors in depreciation.

Here's an example: If your 10-year-old roof gets damaged, replacement cost coverage pays to install a new roof. Actual cash value pays for a 10-year-old roof's depreciated value, which might only cover half the replacement cost.

Yes, replacement cost coverage costs slightly more upfront. But in my experience, it's absolutely worth it. You're insuring your home to truly protect it, not to get a partial payout when disaster strikes.

4. Flood Insurance Is Separate (And You Might Need It)

I need you to remember this: Standard homeowners insurance does NOT cover flood damage.

Pennsylvania has its share of flood risks: from the Susquehanna River to smaller creeks and streams. If your property is in a Special Flood Hazard Area and you have a federally-backed mortgage, flood insurance is mandatory. Even if you're not in a high-risk zone, it's worth considering.

You can purchase flood insurance through the National Flood Insurance Program (NFIP) or private carriers. I've researched options for countless clients, and here's what I've learned: don't wait until hurricane season to think about this. Flood policies typically have a 30-day waiting period before coverage begins.

Check FEMA's flood maps for your area. It takes five minutes and could save your financial future.

5. The Pennsylvania FAIR Plan Is Your Safety Net (Not Your First Choice)

If you've been denied coverage by traditional insurers, Pennsylvania has a backstop: the Pennsylvania FAIR Plan (Fair Access to Insurance Requirements).

Here's the deal: FAIR Plan coverage is basic. It covers your property against fire and some other perils, but it's not comprehensive. You won't get liability protection: that requires a separate policy. It's also typically more expensive than voluntary market coverage.

I only recommend the FAIR Plan after you've exhausted other options. Work with an independent agency like IronClad Coverage to compare multiple carriers first. We have access to numerous insurers and can often find coverage when homeowners assume none exists.

6. Understand Cancellation and Non-Renewal Rules

Pennsylvania has specific rules protecting homeowners from surprise policy cancellations. Here's what you need to know:

First 60 days: Insurers can cancel with 15 days' notice for non-payment or other valid reasons

After 60 days: Cancellation requires 30 days' notice

Non-renewal: You must receive 60 days' notice before your policy expires, with a specific reason provided

These protections give you time to find alternative coverage. But here's my advice: don't let it get to that point. Pay premiums on time, maintain your property, and communicate with your insurer about any changes.

If you do receive a cancellation or non-renewal notice, contact us immediately. Time is critical, and we can help you secure replacement coverage quickly.

7. Budget Realistically for Your Premium

Let's talk money. Pennsylvania homeowners with mortgages typically pay between $1,000 and $1,499 annually for homeowners insurance. Those who own outright generally pay $800 to $999.

Your specific cost depends on dozens of factors: which I'll cover next: but these figures give you a ballpark. When you're calculating your homeownership costs, don't forget to factor in insurance alongside your mortgage, taxes, and utilities.

I always tell clients: if an annual premium seems suspiciously low, scrutinize the coverage. You might be getting bare-minimum protection that won't adequately cover a major loss.

8. Winter Weather Will Impact Your Rate

If you've survived a Pennsylvania winter, you know what I'm talking about. Heavy snow. Ice storms. Freezing temperatures that turn pipes into disasters waiting to happen.

These conditions make Pennsylvania homeowners insurance more expensive than in milder climates. Western Pennsylvania near Lake Erie faces particularly harsh winter weather, which insurers factor into premiums. Frozen pipes, ice dams, and roof collapses from snow accumulation are real risks that cost insurers: and ultimately, homeowners: significant money.

What you can do: Winterize your home properly. Insulate pipes, maintain your roof, keep your heating system serviced, and clear ice dams promptly. Some insurers offer discounts for winter preparation measures.

9. Multiple Factors Determine Your Premium

Your neighbor's insurance rate might be totally different from yours. Here's why:

Location: Proximity to fire stations, hydrants, and emergency services

Home age and condition: Older homes with outdated systems cost more to insure

Coverage amounts: Higher dwelling and personal property limits mean higher premiums

Claims history: Previous claims can increase rates

Home size: Larger homes cost more to rebuild

Construction type: Brick homes typically cost less than wood frame

Security features: Alarm systems, deadbolts, and fire sprinklers can reduce rates

Credit score: In Pennsylvania, insurers can use credit-based insurance scores

Understanding these factors helps you make strategic decisions. Sometimes small improvements: installing a security system or updating electrical wiring: can meaningfully reduce your premium.

10. Consider Add-On Coverages for Complete Protection

Standard homeowners insurance covers a lot, but gaps exist. Optional endorsements can fill them:

Home systems protection: Covers mechanical breakdowns of HVAC, plumbing, and electrical systems

Utility service line coverage: Protects underground pipes and wires from your home to the street

Identity theft protection: Assistance with recovering from identity theft

Scheduled personal property: Extra coverage for jewelry, art, collectibles, and electronics

Water backup coverage: Protection if sewers or drains back up into your home

Equipment breakdown: Coverage for appliance failures

I always review these options with clients. They don't cost much: often $20-50 annually each: but they can save thousands during specific types of losses.

Your Next Step: Compare and Protect

Homeowners insurance isn't one-size-fits-all, and Pennsylvania residents deserve coverage that actually fits their needs and budget.

That's where working with an independent agency makes all the difference. Unlike captive agents who represent one insurer, we compare quotes from multiple top-rated carriers. We find you the best combination of coverage and price: without the sales pressure.

I hope this guide helps you feel more confident about homeowners insurance in Pennsylvania. Your home is likely your biggest asset. Protecting it properly isn't just smart: it's essential for your peace of mind.

Ready to compare homeowners insurance quotes? Reach out to us for a personalized quote from Pennsylvania's top carriers. We'll explain your options in plain English and help you make the best decision for your situation.

Your home deserves ironclad protection.

Comments