Are You Making These 3 Common Homeowners Insurance Pennsylvania Mistakes?

- Jeff Owens

- Feb 23

- 5 min read

Look, I get it. Homeowners insurance isn't exactly the most thrilling topic to think about. You bought your home, you got the insurance your lender required, and you moved on with your life.

But here's the thing I've learned working with Pennsylvania homeowners: the time to think about your coverage isn't when you're standing in your flooded basement or staring at storm damage. It's right now.

I want to share three mistakes I see Pennsylvania homeowners make all the time with their insurance. These aren't small oversights. They're the kind of mistakes that can cost you thousands of dollars when you need your policy most.

Mistake #1: You're Insuring for the Wrong Amount

This is the big one. The mistake that catches more Pennsylvania homeowners off guard than any other.

Here's what happens: You bought your home for $250,000. So you figure you need $250,000 in homeowners insurance, right? Makes perfect sense.

Wrong.

Your home's market value and what it would actually cost to rebuild your home are two completely different numbers. And your insurance company cares about only one of them: the replacement cost.

Think about it this way. Your home's market value includes the land it sits on. But if your house burns down, you still own that land. What you need insurance for is rebuilding the actual structure.

In Pennsylvania, replacement costs can vary wildly depending on where you live. A home in Pittsburgh might have a market value of $200,000 but cost $280,000 to rebuild. Construction costs, local labor rates, building codes – they all factor in.

Here's the rule most Pennsylvania homeowners don't know: you need replacement value coverage of at least 80 percent of what it would actually cost to rebuild your home. If you fall below that threshold, you're underinsured. And when you file a claim, you could face serious out-of-pocket expenses.

What you should do:

Ask your insurance agent to calculate your home's true replacement value

Consider replacement cost coverage, not actual cash value

Review this number annually – construction costs change

Don't base your coverage on your mortgage amount or purchase price

Factor in unique features like custom cabinets, hardwood floors, or additions

I've worked with Pennsylvania homeowners who thought they were fully covered, only to discover they were $100,000 short when disaster struck. Don't let that be you.

Working with an independent agency like IronClad Coverage means we can help you get this number right from multiple carriers. We're not tied to one company's estimates.

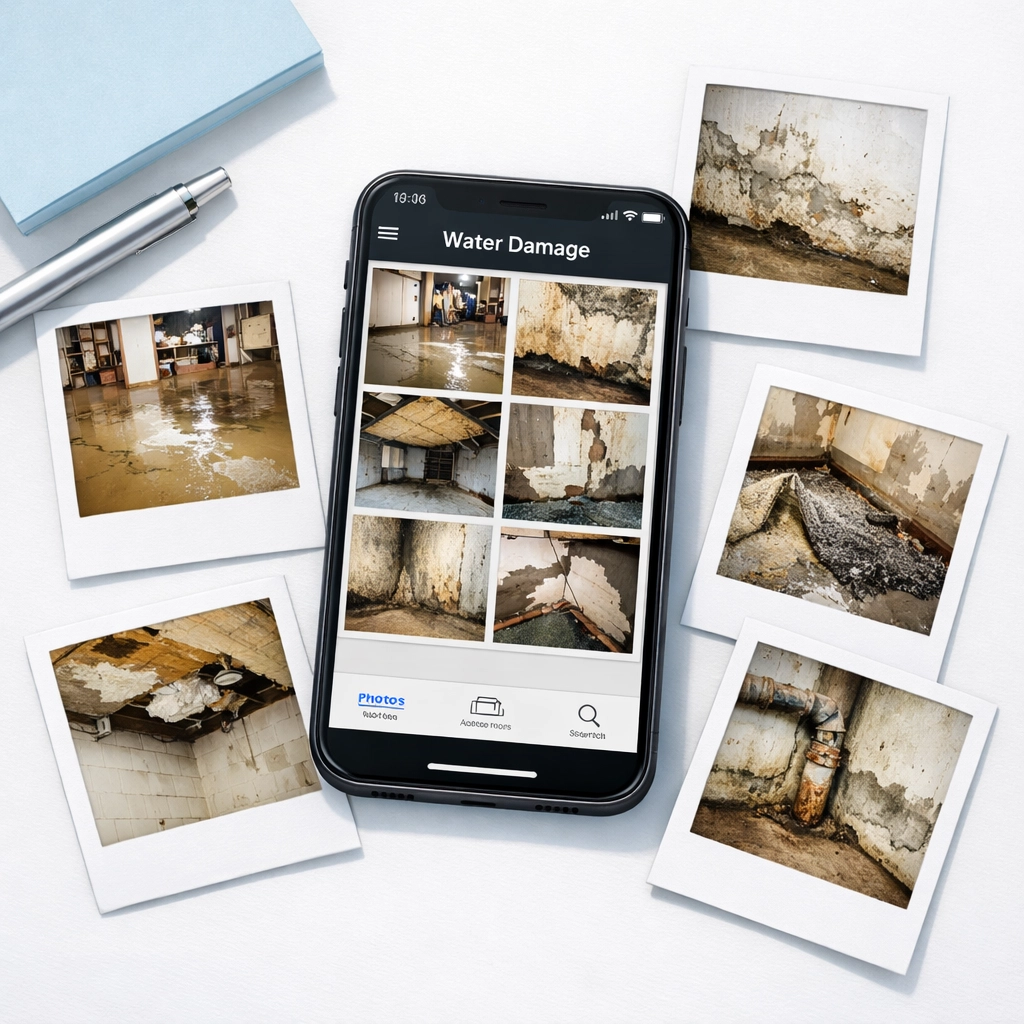

Mistake #2: You're Not Documenting Damage Properly

Let me tell you what happens after a storm rolls through Pennsylvania. I've seen it too many times.

You walk into your basement and find three inches of water. Your first instinct? Grab a mop and start cleaning. Get things back to normal as fast as possible.

I understand that impulse completely. But here's the problem: you just destroyed your evidence.

Insurance claims live and die on documentation. Your adjuster needs to see what happened. They need proof of the damage, proof of what was affected, and proof of value for what you lost.

When you clean up first and document later (or not at all), you're making your own claim harder to prove. You're giving the insurance company reasons to delay, reduce, or deny your payout.

Here's what proper documentation looks like:

Take photos and videos immediately – Before you touch anything, document everything

Capture multiple angles – Get wide shots of rooms and close-ups of damage

Use timestamps – Your phone automatically does this, but make sure

Document every affected item – Even things that seem minor

Save receipts and records – Proof of purchase helps establish value

Keep a detailed inventory – Write down what was damaged and estimated values

Don't throw anything away yet – Your adjuster may need to see damaged items

I know it feels counterintuitive to grab your phone when you should be grabbing a towel. But those five minutes of documentation can make the difference between a fair settlement and a frustrating fight with your insurance company.

One more thing: create a home inventory before disaster strikes. Walk through your house with your phone and film everything. Talk through what things are and when you bought them. Store this video in the cloud. If your home is severely damaged or destroyed, you'll have a record of what you owned.

This kind of preparation makes filing claims so much easier. Trust me on this one.

Mistake #3: You Haven't Actually Read Your Policy

Here's a question: when was the last time you read your homeowners insurance policy?

If you're like most Pennsylvania homeowners I talk to, the answer is "never" or "when I first got it five years ago."

I get it. Insurance policies aren't exactly page-turners. They're dense, full of legal language, and honestly pretty boring.

But not knowing what's in your policy is a mistake that costs Pennsylvania homeowners every single day.

Here's what happens: A pipe bursts in your home. You file a claim. And that's when you discover your policy has a $2,500 deductible, not the $500 you thought you had. Or you find out that water damage from a burst pipe is covered, but your policy excludes the cost of accessing and repairing the pipe itself.

Common coverage gaps in Pennsylvania homeowners insurance:

Flood damage – Standard policies don't cover flooding; you need separate flood insurance

Sewer backup – Often excluded or requires an endorsement

Mold damage – Usually excluded if it's from poor maintenance

Home-based business – Your business equipment probably isn't covered

High-value items – Jewelry, art, and collectibles have sub-limits

Earthquakes – Rarely covered in standard policies

Wind and hail – Some Pennsylvania areas have separate deductibles for these

You need to know your coverage limits, your deductibles, and your exclusions before you need to file a claim. Not after.

Review your policy annually and ask yourself:

What's my deductible, and can I afford to pay it?

Do I have replacement cost or actual cash value coverage?

Are there dollar limits on specific categories like electronics or jewelry?

What disasters are specifically excluded?

Do I have additional living expense coverage if my home becomes unlivable?

Have I made home improvements that increased my home's value?

If you're working with an independent agency like IronClad Coverage, we can walk through your policy with you in plain English. We can compare what different carriers offer and help you understand exactly what you're paying for.

Because here's the truth: the cheapest policy isn't always the best value. Sometimes paying a bit more for broader coverage and lower deductibles gives you real peace of mind.

Get Your Pennsylvania Homeowners Insurance Right

Look, I'm not trying to scare you. I'm trying to prepare you.

Your home is probably your biggest investment. It's where your family lives, where you've built your life. Getting your homeowners insurance right isn't about checking a box – it's about protecting what matters most.

These three mistakes are completely avoidable. You can fix them right now:

Schedule a policy review. Get a replacement value assessment. Start documenting your belongings.

Working with an independent insurance agency means you get objective advice and options from multiple top-rated carriers. We're not pushing one company's products. We're finding you the best coverage for your specific situation.

Want to make sure your homeowners insurance Pennsylvania coverage is actually protecting you? Reach out for a free policy review. Let's make sure you're not making these mistakes.

Your future self – the one who hopefully never needs to file a major claim but is prepared if they do – will thank you.

Stay protected out there!

Comments